PizzaExpress 3 courses �13

PizzaExpress 3 courses �13 O'Neill's free whiskey

O'Neill's free whiskey Zizzi 20% off food

Zizzi 20% off food The cost of car insurance for under-25s is eye-watering. The average price for a 17-20 year-old male is �2,848. Yet there are many ways to help cut this cost.

The cost of car insurance for under-25s is eye-watering. The average price for a 17-20 year-old male is �2,848. Yet there are many ways to help cut this cost.

This is a step-by-step guide to young drivers' car insurance, helping you compare over 100 providers in minutes, with specialised tricks, and dos and don�ts to save every spare penny.

In this guide

Quick links

| Tweet | http://mse.me/young |

Also see 40 Motoring MoneySaving tips to drive down the cost OR

if your vehicle's a different shape, see Cheap Motorbike Insurance

Step 1: Follow the DOs & DON'Ts

DO ensure you always minimise your risk

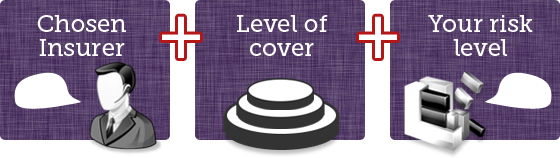

Whether or not you're a young driver, insurance premiums (the payments made to insurance companies) depend on three things:

By reducing an insurer's perception of your risk, you can reduce the price you'll pay.

Car insurance rates are set by actuaries, whose job is to calculate risk. Make sure you're as little of a risk as possible, and you can make big savings by showing an insurer you're not the typical high-risk young driver. Each insurer's price depends on two things. First, the underwriters' assessment of your particular situation; and then the pricing model that dictates the type of customers the insurer wants to attract.

-

Do fit a security device

Any extra security will help. Fitting an alarm or immobiliser (especially one approved by Thatcham) can reduce the bill substantially. -

Do park and drive carefully

Theft and accidental damage add a wedge to insurance costs. If you leave your car in a garage or driveway, it's a big deterrent to theft and means accidental damage is less likely, resulting in a 3-7% drop in insurance costs.

If you have points on your licence, the cost will be higher. While speeding points remain on your licence for four years, insurers usually check for convictions during the last five before they are removed from your record.

One speeding conviction may only affect the price of cover by around 10%, but any more'll bump up the price, with two offences costing around 23% more.

Being caught with a mobile phone is more serious and can double your quote. It can also give you three instant points on your licence, which stay on for four years. Approved hands-free kits are fine if used properly. -

Do reduce your mileage

The less you drive, the cheaper your insurance will be. Where possible, try to reduce your mileage. This may sound trite, but actually the real key is incorporating the extra insurance cost when you make long journeys, not just the cost of petrol compared to taking the bus or train (also read the Cheap Trains guide).

Anecdotally, though many simply get a quote for 10,000 miles per year, MoneySavers have reported that 5,000 is the best figure to use - though we haven't tested this. If you drive your vehicle on business, always declare this rather than just include the business miles as personal, or the policy may be void. -

Do look at additional driving courses

PassPlus: This Driving Standards Agency course is aimed at helping new drivers (within 12 months of passing their test) become more confident on the road. There are six modules: town driving, all-weather driving, driving out of town, night driving, driving on dual carriageways and driving on motorways.

The cost of the course is about �140 but does vary depending on where you live and the instructor or driving school you choose. Yet some local councils offer discounts of up to 40%, usually for those under 25, and in Wales it only costs �20 (check if your council is taking part).

Once you have the certificate some, although not many, insurers discount the price of your insurance. Sadly it's become less and less recognised in the last few years, so the discounts aren't generally that high, and there's a high chance you could get cheaper cover elsewhere.

Drive iQ: This course is provided by the AA and selected independent driving schools - and included within the cost of your lessons - which combines online learning with practical lessons for learner drivers.It covers attitudes and behaviour to driving, rather than just car control skills, and is based around five units which also include motorway and night driving. It says once you�ve passed, you�re eligible for exclusive insurance deals. But check quotes with Drive iQ before you sign up, to see how it compares.

For an optional �50 fee, you will receive a BTEC qualification (equivalent to a GCSE) in Driving Science as well as your licence if you pass.

DON'T assume third party's cheaper than comprehensive

Before we begin, it's important to understand that there are three different types of car insurance: third party, third party fire and theft, and fully comprehensive (full definitions below).

Logically, third party insurance should be cheapest for young drivers as it offers a lesser level of cover than fully comp, yet this isn't always the case. So get quotes for third party and fully comp, just in case it's cheaper. Plus always make sure you check your policy so you know exactly what you are and aren't covered for in the event of a claim.

The rationale might be that insurers see third-party buyers as higher-risk group, as because their car is uninsured (except for damage caused to other cars), they may be more careless with it, so prices are pushed up. To illustrate this, in one low-risk young driver quote we found a �1,500 saving for having comprehensive cover over a third-party only policy. Always check for both.

Third party

The minimum level of cover you need to legally be able to drive on the road is called 'third party'. It used to be the cheapest type of insurance, but fully comprehensive policies can now sometimes be cheaper.

Third party covers you for any damage you cause to another person's vehicle, and gives protection for any passengers in your car.

Therefore, if you're in an accident and it's your fault, you'll have to pay for any repairs to your own car yourself, as your insurance won't cover it. It may be more expensive because it's assumed you care less about your car and are therefore more likely to have an accident.

It's generally the most suitable for those:

- With cars worth less than �1,000

- Aged under 25

- Without a no-claims bonus

- Living in a high risk area

Third party fire and theft

Third party fire and theft has the same level of cover as third party insurance. However, self-evidently, it also offers assistance if your car is stolen or set on fire.

Fully comprehensive

This is the widest level of cover, but can sometimes be the cheapest. The big advantage is that if you have an accident and it was your fault...

You'll be able to claim the cost of repairing your car, and cover personal injury costs, as well as those of other drivers.

The cover also includes accidental damage, windscreen and vandalism, for example if somebody causes damage to your car when it is parked in the street and drives off.

Plus you'll usually (though not always, so do check your policy details carefully) be able to drive other people's cars if you have their permission, although this is likely to only be the minimum level of cover. Sometimes you'll be covered for driving hire cars too.

Fully comp is a good idea if your car is worth more than �1,500, and gets more important the more valuable your car is. Many insurers will only offer fully-comprehensive cover for higher value cars anyway.

There are a few ways of cutting the cost of fully-comprehensive cover. For example, Tesco Value insurance offers a comprehensive policy but has a higher compulsory excess, which lowers the cost. However, this doesn't automatically make it cheapest - make sure you use the comparison sites below to check first.

DO try adding a second responsible driver to your policy

If you're under 25, insurance can cost a fortune. Yet by adding a second driver to the insurance, even if they won't use the car often, it can smooth out the average risk and sometimes reduce the premium. Those with an additional record for driving well are likely to help make bigger savings, but anyone that's in a lower risk category than you can help.

We noticed by adding a 40-year-old family member as an 'occasional' user (not a main driver) to an 18-year-old's policy reduced the premium by approximately �1,000. It won't always work, but it's worth playing with quotes to check.

Don't confuse this with 'fronting', which is illegal - more below.

DON'T put someone else as first driver if it's your car

If it's your car and you'll be the main driver, don't be tempted to put someone else down as the first named driver. Young car owners who list parents as the main driver to cut insurance costs are doing what's called 'fronting' - and IT'S ILLEGAL.

This route may be suggested by well-meaning parents who aren't aware that they're doing anything wrong, and are keen to get a cheaper quote. Yet the consequences can be very serious; it invalidates insurance and can lead to prosecution, so don't do it.

DO tell your insurer about changes and special circumstances

If you haven't got 'normal' circumstances, eg, you've made a claim in the past few years, have a modified car or expect to drive 100,000s of miles a year, tell the insurer. If you don't and then try to claim, even for an unrelated issue, your whole policy may be invalid.

Plus you should also tell your insurer about any changes. This is crucial as it reduces potential problems in the event of a claim, even if it's just your address. Trying to get insurance after you've had a policy cancelled due to a fraudulent claim is very difficult, very expensive and will follow you for the rest of your life.

A change in circumstances includes moving jobs, as insurers believe this can affect your risk. Scandalously, the unemployed often (though not always) pay higher rates for their car insurance, so do inform your provider if you're out of work but also do the full combine comparison site checks below to see where you can get the cheapest cover.

DON'T pimp your car

Sexy it might be, MoneySaving it ain't. The more changes you make to your car, barring security ones, the more you'll be charged.

Always make sure you inform your insurer of any modifications to your car, whether you made them or not, or it may invalidate your policy. A modification is anything that isn't part of the standard vehicle specification, including factory-fitted optional extras such as alloy wheels.

DO work out how much you'd really claim for

It's worth considering going for a policy with a higher excess (the amount of any claim you need to pay yourself). Many people will find claiming for less than �500 of damage both increases the future cost of insurance and can invalidate no-claims bonuses, meaning it's not always worth making a claim.

So why pay extra for a lower excess? A few policies will substantially reduce premiums for a �1,000 excess, so try this when getting quotes. The downside of this is if you have a bigger claim you'll have to shell out more, so do take this into account.

DON'T be tempted to lie

With insurance, remember - the golden rule is:

If you've read these tips and thought, "it's easy to lie about this", then of course, you're right.

Yet lying on your insurance form is fraud. It can lead to your insurance being invalidated and, in the worst case, a criminal prosecution for driving without insurance. Don't do it.

DO try multi-car policies if you live with parents

If you've two or more vehicles between friends or family members in your household (vans can be included in this but bikes usually aren't), some providers offer discounts if you insure them all together. Comparison sites don't have the technology to do these searches, so you need to compare manually.

First, use comparisons for each car separately. The discounts are usually around 10%, so often it's likely just finding the cheapest standalone insurer will win anyway. So always do a comparison first (see combine comparison sites below), then try the deals below to compare.

Get all cars on one policy. Cover two or three cars and Admiral* will give up to 14% discount, cover four or five and you could get up to 23% discount. All cars will then be covered on one policy so the renewal date will be aligned to end at the same time.

Separate policies but still get the discount. Other insurers allow cars to have separate policies but give a discount as long as the vehicles are in the same household.

Privilege* gives up to 10% off, Direct Line* 10% off, Churchill* (which also covers named drivers on another Churchill policy) up to 15% off. Aviva* isn't included within comparison sites but will give up to a 33% discount if you cover more than one vehicle.

DON'T forget that car type impacts on insurance cost

The combination of popularity, engine size and value all have an impact on car insurance cost. It's worth considering this when you buy; insuring a super-powerful beast of an SUV for a 17-year-old would cost enough to make Bill Gates weep.

DO SEE IF YOU CAN SAVE If you're a man - EVEN IF NOT AT RENEWAL

These techniques should slash your costs. Yet even so, for some young drivers, car insurance will remain unaffordable. You need to decide - is it really worth it?

There's another quick tip to lower your costs: tweaking your job description could save you cash. Insurers decide prices depending on historic risk assessments, and your occupation plays an important part in this. To help, we've built a fun Car Insurance Job Picker tool to show the riskiest jobs and see if small tweaks to your job description could save you cash.

You may also save on insurance if you're in a more stable relationship, ie, if you're living with a partner rather than listed as single.

Step 2. Correctly combine comparison sites

Comparison sites zip your details to hosts of insurers' and brokers' websites, scraping their data off the screens to report back the cheapest. So be aware they often feed your personal details to insurers.

They don't all compare the same sites, so the best strategy's to combine them. We've analysed the comparison sites, using a large range of monthly data, primarily focused on which ones produce the cheapest results. For drivers aged 25 or over, see our Cheap Insurance Guide.

However, as well as the price data, we have also conducted separate research to see if quotes from comparisons match up to the prices on insurer�s own websites, how consumer-friendly the quote process is, and the speed at which the comparison delivers results. These have been fed in to help us decide the best to use (see How the order is picked ) :

1. MoneySupermarket* Gets a cheap quote 67% of the time (in our sample)

Plus a quality rating of 6/10 in our survey of 'soft features'

- Price for add-ons clearly displayed: Yes

- Received marketing calls when requested not to: No

- Prices quoted match insurer's site: 50/50

- Excesses match what was asked for: No

- Tick-box for marketing calls: Opt-out

- Add feedback: MoneySupermarket

try it*

try it* 2. ...plus Confused.com*Increases chances of cheapest quote from sample to 84%

Plus a quality rating of 6/10 in our survey of 'soft features'

- Price for add-ons clearly displayed: Yes

- Received marketing calls when requested not to: No

- Prices quoted match insurer's site: 50/50

- Excesses match what was asked for: No

- Tick-box for marketing calls: Opt-out

- Add feedback: Confused.com

Check the big 'uns they miss ...

Aviva*: Buy online and get a discount of up to 20%. Also, get up to a third off with Aviva Multi Car when you add a second car.

Aviva*: Buy online and get a discount of up to 20%. Also, get up to a third off with Aviva Multi Car when you add a second car.

Direct Line*: Worth trying as it doesn't appear on comparison sites. Also, see Direct Line Together* for details on getting 10% off every car, or any other Direct Line product, in your household. Quotes can be obtained up to 90 days ahead.

Direct Line*: Worth trying as it doesn't appear on comparison sites. Also, see Direct Line Together* for details on getting 10% off every car, or any other Direct Line product, in your household. Quotes can be obtained up to 90 days ahead.

Top three samples likely to give a cheap quote 88% of time.

Approx time to get a quote:

7 mins

try it*

try it*3. ...plus Google* Increases chances of a cheap quote from sample to 88%

Plus a quality rating of 7/10 in our survey of 'soft features'

- Price for add-ons clearly displayed: Yes

- Tick-box for marketing calls: Opt-in

- Received marketing calls when requested not to: No

- Prices quoted match insurer's site: 50/50

- Excesses match what was asked for: No

- Add feedback: Google

try it*

try it*4. ... plus Tesco Compare* Increases chances of cheapest quote from sample to 94%

Plus a quality rating of 4/10 in our survey of 'soft features'

- Received marketing calls when requested not to: No

- Prices quoted match insurer's site: 50/50

- Excesses match what was asked for: 50/50

- Price for add-ons clearly displayed: No

- Tick-box for marketing calls: Opt-out

- Add feedback: Tesco Compare

Total...

(close to) 100% chance of cheapest quote,

based on insurers comparison sites cover.

5. Boost chances to nearly 100% Try to really nail down all the quotes

If you still haven't found a deal you're happy with, or want to push the envelope, there are some more options to try.

Try these comparison sites if you have time - each takes around 5-10 minutes: Comparethemarket*, Gocompare*, QuoteZone*.

Based on a full price survey carried out roughly every month, last done in May 2013 using April 2013 data, and also a separate quarterly qualitative survey, last carried out in April 2013..

Comparison sites have attempted to tackle the market by offering quick cashback if you compare then get a policy through them. While it doesn't pay nearly as well as some hidden cashback deals (see step 4), it could still be enough to make a difference.

MoneyExpert:

MoneyExpert:

This site pays �25 cashback, but currently its sister, SimplySwitch, is bumping the offer to �40 if you go via its site and enter the code SIMPLYCAR. Important: How to get the cashback

The cashback must be claimed between 14 and 30 days after the policy starts (ie, not when it was purchased). If you leave it more than 30 days, you won't get the cash, so diarise this carefully.

It must be claimed from MoneyExpert (not MoneySavingExpert) specifically by the car insurance policyholder using the cashback claim form, plus it's not available if you're in Northern Ireland or the Channel Islands - read the full T&Cs;.

With both the process isn't that straightforward, nor without potential pitfalls, also be aware neither site lets you opt out of further marketing, so you are likely to get follow-up phone calls and emails.

If you have any problems getting the cashback email carinsurance@moneyexpert.com or phone 0800 011 1395 (it says it's for the energy team, but select option 2 for customer services).

Important: read this before going for it.

As well as the slightly complex claim procedures, you should never see this as a done deal, only as an added bonus. Another thing in common with normal cashback sites - never count the cash until its in your bank account. Your primary aim should always be getting the cheapest policy.

It's important to be aware that the cashback is coming from the comparison sites, not the insurer, so getting the cashback does rely on their ability to pay.

These sites include far fewer insurers than the main comparison sites above (though they do add around 30 new providers, so are worth checking on top) but they argue the cashback they give makes up for that - provided you jump through the hoops to get it.

MoneyExpert has set its default excess to �400 and includes some assumptions, so be careful to check the quotes are right for you.

Always double-check the policy terms...

Once you've found the cheapest from the screenscrapers, make two important checks:

-

Double check the quotes

Click through to the insurance provider's own website to double check the quotes, as to speed up searches some comparison sites make a few assumptions (see what to check). - Examine the policy's coverage

Check whether it's suitable. So if you want "free car hire" if your car is being fixed, is it included?

Plus while you're there, it's worth playing with the policy details to see if you can finesse the price down. Look at the excess, and whether adding drivers cuts the cost.

This tool by Find allows you to check the coverage of two different polices side-by-side.

What happens if my insurer goes bust?

Insurance providers regulated in the UK are covered by the same Government-backed Financial Services Compensation Scheme (FSCS) as banks, meaning if they go into default, you're protected.

A number of insurers - particularly those who offer telematics pay-when-you-drive cover - are based in Gibraltar. However, a special FCA rule says these policies have the same protection as those from UK-based insurers. Specifically... "the UK requires all EEA (European) insurers... to participate in the FSCS in the same way as all insurers that are directly authorised by the FCA."

In the unlikely event a regulated insurer goes bust, the FSCS will try to find another provider to take over or issue a substitute policy. However, if you've ongoing claims, or need to claim before a new insurer is found, the FSCS should ensure you're covered. For more see the Insurance section of the Savings Safety guide.

Step 3: Specialist young driver policies

Once you�ve tried the comparison sites, it's time to check specialist young driver policies to see if they undercut them.

If you are a careful driver who doesn�t cover many miles and drives during off-peak hours, you could see a reduction in the premium.

Due to the non-conventional nature of these policies, getting a firm price will often involve getting a calculator out.

Pay when you drive

A tracking device is fitted to your car to monitor when you drive - so the more you drive, the more you pay (though of course, it's also likely to depend on your personal risk profile).

A tracking device is fitted to your car to monitor when you drive - so the more you drive, the more you pay (though of course, it's also likely to depend on your personal risk profile).

Coverbox. A 'pay as you drive' scheme from Coverbox* has per-mile charges that vary according to the time of day or night when you drive.

For low mileage drivers these can cut costs, especially if you don�t drive at night (11pm - 5am) when the costs per mile jump. While not specifically for young drivers, at times it does offer some drivers under 30 cashback of �50 (details will be on your quote if you qualify).

iKube. Alternatively, iKube* is aimed at 17-25 year olds who don't often drive between 11pm and 5am; there's an extra fee for driving outside the set hours, making the cost prohibitive if you do so.

Insure The Box. With Insure The Box, you can pick either a 6,000 or 8,000 mile per year policy for your premium, and then you can earn extra miles by driving safely - or buy more online if you need to during the year.

Pay how you drive

Here, GPS or tracking devices monitor how you drive. Of course, even then, the price still depends on your personal risk profile.

Here, GPS or tracking devices monitor how you drive. Of course, even then, the price still depends on your personal risk profile.

AA. The AA's Drivesafe policy uses GPS technology and considers four factors: speed, anticipating traffic, following the landscape and 'where and when'.

Based on these factors, and a few more, your premium could adjust accordingly though you are able to log into a 'driving dashboard' to check Drivesafe scores and reports.

The Drivesafe box also doubles up as a theft tracking device.

Co-op. The Co-op's* young driver insurance fits a box into 17-24-year-olds' cars to monitor acceleration, braking, cornering and time of driving. It then charges for insurance every 90 days, taking into account any discounts or loadings.

The price of the insurance can vary, depending on how well the car�s been driven � and severely bad driving could see your insurance cancelled.

See the MSE News story Young drivers 'pay how you drive' insurance unveiled for more.

Specific young driver brokers

While comparison sites are very good for people with normal situations, for others they can underperform. Swinton's Young Driver* insurance is worth checking out, as it searches a panel of young driver and student car insurance providers.

Until further notice, Swinton* is giving a �40 cashback (you must use the promotional code PMWTDR663) plus an online discount of up to 25%.

Other brokers providing for young drivers include A Plan, Thames City, Only Young Drivers, Adrian Flux and Endsleigh (best to call for quotes, as not all offer these online).

Or try speaking one-on-one to a local insurance broker about your individual circumstances to see if they can find you a decent policy (search on the British Insurance Brokers' Association website).

Learner driver insurance

If you're a learner, it often means being added to parents' or friends' car insurance as an additional driver which can up the cost, and put no claims bonuses at risk.

If you're a learner, it often means being added to parents' or friends' car insurance as an additional driver which can up the cost, and put no claims bonuses at risk.

However, it is possible to get specific policies just for the provisional driver which protect this, such as Provisional Marmalade* and Endsleigh*.

Provisional Marmalade also has a logbook scheme which you can complete to get a �100 discount if you move to Young Marmalade when you�ve passed.

-

Free insurance with a new car

If, after you�ve tried everything, you still need to shell out thousands of pounds for car insurance, it may be worth looking at policies that effectively wrap the insurance up with a car purchase.

Some dealers and manufacturers do this as a temporary promotion from time to time, so it's worth keeping your eyes open for these. There�s also:

-

Young Marmalade: With Young Marmalade* you get the insurance policy alongside low-risk new or nearly new cars on a two to five-year hire purchase or personal contract plan.

This can bring the insurance cost down dramatically, but obviously, you're buying a car at the same time. Do the numbers very carefully before signing up, though it can work out cheaper in the long run for some.Young Marmalade cars also include an intelligent tracking scheme that allows you to monitor your driving and correct issues such as excessive braking, cornering, acceleration or speed. The cost savings for good drivers are built into your starting price, so it can be increased if your driving is poor.

Don't miss out on updates to this guide Get MoneySavingExpert's free, spam-free weekly email full of guides & loopholes

Step 4: Grab hidden cashback, discounts & haggling

By now you'll know the cheapest available provider, yet you may be able to cut the cost even further.

The top cashback deals

Once you know who your cheapest provider is, you need to check there aren't any hidden cashback deals, these can be as high as �100. If your second or third cheapest quotes weren't too much more expensive, see if cashback's available for them too and find the overall winner.

The step-by-step list below takes you through a variety of options to improve your deal.

Check 1: Cashback websites

These sites carry paid links from some retailers and financial services providers; in other words, if you click through them and get a product, they get paid. They then give you some of this cash which means you get the same product, but a cut of its revenue.

Don't choose based only on cashback, see it as a bonus once you've picked the right cover.

Those new to cashback sites should ensure they read the Top Cashback Sites guide for pros and cons before using them.  Otherwise use the Cashback Sites Maximiser tool to find the highest payer for each insurer.

Otherwise use the Cashback Sites Maximiser tool to find the highest payer for each insurer.

Things you need to know before doing this...

- Never count the cash as yours until it's in your bank account. This cashback is never 100% guaranteed, there can be issues with tracking and allocating the payment, plus many cashback sites are small companies with limited backing, and you've no protection if anything happens to them.

- Withdraw the cashback as soon as you're allowed. Money held in your cashback site account has no protection at all if that company goes bust, so always withdraw it as soon as you're eligible.

- Clear your cookies. While it shouldn't be a problem, if you've used comparison sites beforehand, there is a minor risk that the cashback may not track due to cookies - so it's good practice to clear those first (read About Cookies).

Check 2: Get cashback via comparison sites

If cashback sites don't list your insurer, then a couple of comparison sites pay cashback if you compare then get a policy via their sites.

MoneyExpert pays �25 (although currently its sister site, SimplySwitch*, is topping the offer up to �40 if you go via its site and enter the code SIMPLYCAR).

Again though, it's more important to get the right policy than a bit of cashback, so make sure you've done that first. However, you must make sure you tick all the right boxes to claim this cashback, and understand the comparison sites pay this bonus directly - not the insurers - so you're reliant on their ability to pay. Please read the quick cashback section above for full pros and cons.

Check 3: Special deals

If you can't get cashback it's worth noting a few companies have special deals not mentioned by comparison services. These currently include (listed alphabetically):

|

Aviva* offers up to 20% off your premium if you buy online. Also, get up to a 1/3 off with Aviva MultiCar when you add a second car. |

Insurance broker Be Wiser is giving free RAC membership for policies bought via its website. |

If you buy via Confused.com*, you'll get 1,000 Nectar points. A claim form needs to be completed within 60 days of taking out the policy to validate your points. Other T&Cs; apply. |

If you're a NatWest current account holder, you'll receive a 15% discount for taking out a new car insurance policy. Also, if you're already a NatWest home insurance policyholder, you'll get a further 10% off. |

Nectar cardholders who buy a Sainsbury's* comprehensive motor policy by 3 Jun 2013 can save up to 33% on the premium and get double Nectarpoints for two years on Sainsbury's shopping and fuel. See the T&Cs; . |

Until further notice, if you buy a motor policy from Swinton*, and enter the code PMWTDR663, you'll get �40 cashback. |

Haggle on your car insurance!

The car insurance market is very competitive and companies are desperate to retain business - but never just auto-renew.

Insurers love auto-renew, as it's a fine for apathy where they hoick the premium knowing you'll pay. If a policy has automatically renewed, getting out of it usually means charges and fees, so don't get caught out.

Once you've got your overall cheapest price, get on the phone and try to haggle as your renewal is a starting point. There's often massive price flexibility, but be fully armed with the screenscrapers' cheapest quotes and any available cashback first.

The first port of call should be your existing insurer. If it can beat or even match the best quote it saves the hassle of switching policy. If that doesn't work and you're still in the mood, take it to a broker. For more haggling tips, read the full Haggle On The High Street guide and 2013's top 10 firms to haggle with.

Have you used this guide's techniques to save on your car insurance? If so, please feed back on the price you found in the Young Drivers' Insurance Savings forum discussion.

Step 5: Remember next year

Fortunately, providing you drive well and don't have any accidents, your insurance premium should get cheaper after the first year. However, don't automatically stick with the same provider - it may not still be cheapest.

Apply for cover from your existing insurer as a new customer and it's likely you'll be given a cheaper price. This is because car insurers, like any company, will happily profit from apathy if they can.

Insurers must send out renewal notifications at least 28 days before renewal, though this doesn't leave much time, and you can end up rushing to try to find a cheaper price.

To avoid being forced to decide quickly, diarise a warning 45 to 90 days before your renewal date, so there's plenty of time to sort out a new provider. Alternatively use the free Tart Alert which sends a reminder text or email.

Get paid to be a mystery shopper

You could also sign up to Consumer Intelligence, a consumer research company, which pays several hundred people a month near renewal up to �50 to carry out comparisons. Importantly, you don't need to buy insurance from any of the companies you've contacted. See the It's a mystery forum thread for full details.

Young drivers' car insurance Q&A;

Why is car insurance so expensive for young drivers?

Unfortunately there are several reasons for this. Young drivers are less experienced than older road users, bringing them into a higher risk category with insurers. Less experienced drivers are more likely to have more accidents, and therefore put in more claims to their insurers - so insurance companies make their premiums more expensive to compensate.

Yet by driving carefully you can help offset this and lower your premium - see above for more.

Should I take a monthly payment plan?

Beware 'pay monthly' options - usually the insurer just loans you the annual cost and then charges interest on top at hideous rates. As the average cost for a 17-20 year old male is �2,848, paying by instalments can easily add another �300 to your premium.

So either pay in full, or if you can't afford it, try to borrow the money elsewhere more cheaply (ideally on a 0% credit card for spending, ensuring your repayments are big enough to clear it within a year.)

I'm not driving my car for a bit, does it need to be insured?

Yes - cars must be insured unless declared off-road. The Continuous Insurance Enforcement scheme means all cars must be insured - even if no one drives them. The aim's to crack down on two million uninsured drivers by matching up the database of cars and insured drivers.

The only way out is to apply for a Sorn (Statutory Off Road Notification) declaring your car will never be driven. Ensure you search for the new cheapest in advance of renewal, or you'll end up just auto-renewing to stop the fine.

Am I covered to drive others' cars on my insurance?

If your insurance allows it, driving someone else's car instead of yours can be a way to cut mileage. Check your policy details carefully to find out if you can.

If you have fully comprehensive insurance then often, although not always, it includes what�s called "driving other cars" cover. This provides you with third party cover whilst reducing your mileage and therefore the cost of your own policy.

Would it be cheaper for me to just get a motorbike instead?

Generally, insurance is a lot cheaper for a moped or motorbike than for a car. Plus, some insurers may put any no claims bonus from bike insurance on your car insurance too if you later get your car insured with them. Yet do take safety into account as a new driver - if you're in an accident, you're better-protected if you're in a car. See the Bike Insurance guide for more.

What's the difference between a screenscraper and a broker?

Brokers and screenscrapers may seem like they're doing a similar job, as each search a number of different insurers; yet they're radically different beasts. A good analogy for this is to compare it to searching for the cheapest loaf of bread.

Individual insurers are like bakers, your choice is simply to buy its cheapest loaf that suits.

Brokers are like supermarkets; they stock a range of bakers' loaves and the price charged depends on their relationships with suppliers.

Screenscrapers are like sending someone round supermarkets and bakers to note all their prices.

Are there any ways to get to a no-claims bonus faster?

Some schemes do offer an accelerated no-claims bonus - giving you a year's no-claims bonus after 10 months - such as Admiral's* Bonus Accelerator.

MSE's forumites have also suggested another tip. If you've previously been insured as an additional driver on, for example, your parents' policy, call your insurer and ask if they'd be willing to take this into account for a no claims bonus. Some insurers do this, including Direct Line*. See the Great Young Drivers Insurance Savings Hunt discussion for more tips and tricks.

Must I inform my insurer if I have an accident but don't claim?

If you have an accident, and damage someone else's car, but decide to cover the costs yourself, then strictly speaking, you should still tell your insurer about it.

Many don't, thinking it will increase premiums, yet a problem may arise if you have a second accident and it is found to be related to work undertaken for the first. If this happens it would most likely result in the claim not being paid, rather than the insurance being cancelled or being reported for fraud. But could still end up costing you �1,000s.